Search Blogs

April 2, 2026

Florida Premiums Drop Amid Post-Reform Stability, New Triple-I Insurance Brief Shows

April 2, 2026

57% of Homeowners Make Financial Sacrifices to Afford Coverage, Insurify Finds

Premium Growth Outpaces Inflation

Rising premiums are a key factor behind these financial adjustments. According to Matt Brannon, senior economic analyst at Insurify, the typical home insurance premium has increased nearly three times as fast as inflation over the past four years. Premiums rose 46% during that period, compared to a 16% increase in inflation. Two primary drivers are contributing to higher costs: increased rebuilding expenses and growing exposure to extreme weather events. Brannon noted that construction costs surged during the COVID-19 pandemic due to supply chain disruptions. As a result, replacement costs have increased significantly. A home that cost a certain amount to rebuild in 2019 may now require up to 40% more to insure at full replacement value. At the same time, insurers are responding to heightened catastrophe risk. The U.S. experienced 23 billion-dollar weather disasters in 2025, the third-highest total on record, following 2023 and 2024. As risk increases, insurers often adjust pricing to account for higher potential losses.Insurance Costs Often Overlooked in Homebuying

Despite rising premiums, many buyers are not factoring insurance into their home purchase decisions early enough. Insurify’s data found that nearly half of surveyed homeowners did not consider insurance costs when buying their home. Brad Spurgeon, owner and CEO of Brad Spurgeon Insurance Agency in Texas City, Texas, said insurance is frequently overlooked during the buying process. “Insurance often is the last thing on homebuyers' minds and can catch them off guard at closing,” Spurgeon said. “Most of the focus is on the mortgage payment, taxes, and HOA fees, not insurance.” Industry professionals note that evaluating insurance costs earlier in the process can help avoid unexpected increases in total housing expenses. In some regions, particularly those exposed to natural disasters, insurance pricing can significantly affect monthly payments. Brannon pointed to Florida as an example, where insurance and flood coverage can materially impact affordability. Buyers considering properties in higher-risk areas, such as those prone to hurricanes, may face elevated premiums. Understanding these costs before submitting an offer can help reduce the likelihood of last-minute adjustments, such as increasing deductibles or reducing coverage levels.Strategies to Manage Rising Costs

While premiums continue to rise, several approaches may help homeowners manage costs. One recommendation is to regularly compare insurance quotes. Brannon advised homeowners to review rates from at least three insurers every six months. However, he emphasized the importance of comparing equivalent coverage limits and deductibles to ensure accurate evaluations. Discounts also remain a potential avenue for savings. Insurers may offer reductions for policyholders who bundle coverage, install security systems, pay premiums in full, or meet certain eligibility criteria such as military service or age. Some discounts may not be widely advertised, making it important to inquire directly with insurers or agents. Property-level risk mitigation can also influence premiums. Upgrades such as fortified roofs or hurricane shutters may reduce the likelihood of damage, thereby lowering insurers' perceived risk. Some states offer financial assistance programs for these improvements, and in certain cases, insurers are required to provide discounts for qualifying upgrades. As premiums continue to increase, these strategies may play a larger role in helping homeowners maintain coverage without making significant financial trade-offs. Stay informed and ahead of the curve — explore more industry insights and program opportunities at ProgramBusiness.com.

April 2, 2026

Farmers Introduces Capital-Backed Agency Model as Part of 2026 Growth Strategy

Farmers Insurance has launched a new recruitment initiative aimed at entrepreneurs with significant capital as the company works to appoint nearly 1,700 agency owners in 2026.

The effort centers on the newly introduced Elite Owner Program, which targets applicants with at least $500,000 in capital. The program is designed for individuals who can establish agencies at scale from the outset and is part of a broader strategy to expand the company’s distribution network.

Elite Owner Program Structure

The Elite Owner Program offers tiered participation levels, including Gold, Platinum, and Diamond. Each tier provides varying levels of operational support, such as dedicated service channels, startup assistance, and marketing resources.

According to Farmers, the structure combines owner capital with company support to facilitate accelerated policy sales and premium growth compared with other agency appointment pathways.

The program operates alongside existing recruitment channels, including the Retail and Acquisition programs, which allow candidates to start new agencies or purchase existing ones. Additional pathways, such as the Financial Services Agent and Business Insurance Agent programs, also remain in place.

Recruitment Goals and Distribution Strategy

Farmers stated that the recruitment initiative supports its broader goals of organic growth, modernization of its distribution model, and expansion of market share. The company also noted that increasing its agency footprint is intended to strengthen its presence in local communities.

Ken Walton, president of distribution at Farmers, said the company is increasing its focus on entrepreneurial agency ownership.

"We're doubling down on the entrepreneur model to drive our next chapter of growth," Walton said. "By onboarding 1,700 new agency owners, including an Elite tier of well-capitalized business leaders seeking to build or expand their portfolio, we'll be injecting fresh energy into our distribution force."

Walton added that agency owners retain the flexibility to operate independently while receiving support from Farmers. This includes the ability to sell select non-Farmers branded products.

Recruitment Activity Trends

Through February 2026, new agent appointments increased 34% compared with the same period a year earlier. The company also reported that its recruiting pipeline nearly doubled year over year.

Farmers indicated that these figures reflect continued recruitment activity throughout the year.

Existing Structural Framework

The current recruitment push builds on prior structural changes. In 2024, Farmers implemented its district manager model across all US regions. The model includes a mentorship framework designed to support new agency owners as they establish and grow their businesses.

The planned addition of nearly 1,700 agency owners would represent one of the largest single-year increases in the company’s 95-year history.

Application Process

Prospective agency owners can apply through Farmers’ recruitment platform. Applicants may be contacted by a district manager or a member of the Elite Owner Program recruiting team as part of the evaluation process.

Related Underwriting and Capital Developments

Separately, Farmers has made recent adjustments to its underwriting and capital strategy.

In November 2025, the company announced it would remove a cap of 9,500 new homeowners policies per month in California. It also began marketing to approximately 300,000 consumers in areas identified by the California Department of Insurance. Additionally, Farmers filed for a 6.99% average statewide rate increase and proposed increasing its Home and Auto discount to 22% from 15%.

In another development, Farmers completed a $400 million catastrophe bond through Topanga Re Ltd. The transaction included $300 million in Class A notes and $100 million in Class B notes. Both note classes provide four years of per-occurrence and indemnity-based protection against U.S.-named storms, earthquakes, severe weather, and fire. The coverage is part of the company’s reinsurance program.

Get the latest insurance market updates and discover exclusive program opportunities at ProgramBusiness.com.

April 1, 2026

NAIC Launches Nationwide Homeowners Data Call as Market Pressures Intensify

April 1, 2026

Hurricane Planning Tool Faces Uncertain Access Ahead of 2026 Season

Emergency planners across the United States may soon face uncertainty regarding access to a key hurricane planning tool, according to a recent CNN report.

HURREVAC, a web-based platform used by meteorologists and emergency managers, supports critical decision-making before and during hurricanes. FEMA owns and funds the tool, while the U.S. Army Corps of Engineers administers it through an interagency agreement. That agreement has not been renewed, which has delayed the contract tied to the system.

Officials within FEMA, along with external meteorologists and the International Association of Emergency Managers, have warned that access to the system could be interrupted in the near term.

HURREVAC allows users to simulate both historical hurricanes and potential future storm scenarios. Emergency planners rely on these simulations to evaluate evacuation timing, storm surge impacts, and response strategies. The system also supports joint training exercises between the National Weather Service and emergency management agencies.

The platform integrates storm surge data through the National Weather Service’s SLOSH modeling tool. Access to that data could also be affected by the same contract lapse.

The timing of the situation coincides with the period when many agencies begin hurricane preparedness training. The 2026 Atlantic hurricane season is about three months away.

Brian LaMarre, a former chief meteorologist for the National Weather Service in Tampa and now a private consultant, said the tool plays a central role in preparedness efforts. He noted that planners use HURREVAC to simulate storms of varying intensity and direction to assess how surge levels and evacuation needs may change across different communities.

The simulations help local officials evaluate evacuation routes, timing, and other logistical factors. These exercises are designed to support decision-making based on both forecast data and historical trends.

In a March 18 statement, the International Association of Emergency Managers said disruption to the tool would limit access to storm surge visualizations, training modules, and transportation modeling. The organization represents more than 6,000 emergency managers nationwide and noted that the current contract was set to run through late March.

A FEMA spokesperson stated that the contract will be extended and that the system remains operational. The agency said there is no interruption in service and emphasized that HURREVAC remains available to emergency management partners.

However, LaMarre said he was not aware of any confirmed extension at the time of reporting.

During hurricane season, officials also use HURREVAC to analyze real-time data. The platform allows users to overlay the hurricane track cone of uncertainty onto local maps, helping planners assess how potential shifts in a storm’s path could affect specific areas.

According to LaMarre, if access to the system is interrupted, it could reduce the time available for training and limit the tools available for interpreting incoming storm data.

Get the latest insurance market updates and discover exclusive program opportunities at ProgramBusiness.com.

April 1, 2026

California Considers Construction Insurance Role to Support Factory-Built Housing

California lawmakers are exploring a new approach to address the state’s housing shortage. A recently introduced legislative package focuses on expanding factory-built housing, including a proposal that would involve the state in construction insurance.

Per Cal Matters, Assemblymember Buffy Wicks of Oakland, along with a bipartisan group of legislators, introduced several bills to encourage cost-cutting construction methods. The package places particular emphasis on factory-based building, where homes are constructed off-site and transported for installation.

Supporters of factory-built housing point to several potential benefits. These include faster construction timelines, safer working conditions, and lower overall costs. These efficiencies are expected to help make housing more affordable. However, despite long-standing interest in the concept, the industry has not reached large-scale adoption. Industry advocates cite regulatory and financial barriers as key challenges.

One proposal, Assembly Bill 2166, takes a different approach from the rest of the package. Authored by Wicks and Assemblymember Juan Carrillo of Palmdale, the bill aims to provide insurance guarantees for developers and lenders working with factory-built housing. While details remain limited, the bill would position the state as a reinsurer in certain situations.

This approach would mark a departure from previous housing policy efforts in California. Tyler Pullen, a researcher at the Terner Center for Housing Innovation at UC Berkeley, said the concept is new at the state level. He noted that similar ideas have emerged in discussions with industry stakeholders, though the proposal remains complex and open-ended.

Construction projects often carry significant financial risk. Cost overruns, project delays, and legal disputes are common concerns. To manage these risks, stakeholders rely on financial tools such as surety bonds. These arrangements allow an insurer to guarantee payment if a contractor or subcontractor fails to meet obligations.

Surety bonds provide reassurance to developers and lenders. According to Michael Merle, business development director at Autovol, a bonded project reduces financial exposure if a part of it fails. However, obtaining a bond can be difficult for factory-based builders, especially newer companies without an established track record.

The bill identifies a “self-reinforcing cycle” affecting the industry. Developers and lenders often require bonding due to concerns about factory reliability. At the same time, factories struggle to secure bonding without proven financial performance. This dynamic can limit opportunities for newer manufacturers and restrict industry growth.

Under the proposed legislation, the state would partially back surety bond payouts in certain extreme cases. The goal is to increase insurer confidence, which could lead to broader bonding availability. In turn, developers may feel more comfortable engaging with factory-built housing providers.

The concept resembles existing guarantee programs in other sectors. Federal entities such as the U.S. Department of Veterans Affairs, Fannie Mae, and Freddie Mac guarantee mortgages to encourage lending. The Small Business Administration provides surety bond guarantees for small businesses. California currently operates a loan guarantee program for health care facility construction, though it does not extend to housing.

Industry response to the proposal has been mixed. Some stakeholders view the measure as a way to support emerging manufacturers. Others question whether it addresses the most pressing barriers.

Ryan Cassidy, vice president of real estate at Mutual Housing California, expressed skepticism about the approach. His organization already uses factory-built housing and works with established manufacturers. He suggested that direct financial support for projects may be more effective than insurance-related incentives.

Merle noted that larger, established factories often have fewer challenges obtaining coverage. However, newer companies with limited project history face greater difficulty securing bonds. The proposal could primarily benefit those newer entrants.

Lawmakers will consider the bill in a legislative committee hearing scheduled for late April. Several details remain unresolved, including the extent of the state’s financial exposure.

Pullen said the proposal is intended to support early adoption of factory-built housing. Over time, he indicated that private insurers may become more willing to provide coverage without state involvement. For now, the approach's effectiveness remains uncertain.

Get the latest insurance market updates and discover exclusive program opportunities at ProgramBusiness.com.

March 31, 2026

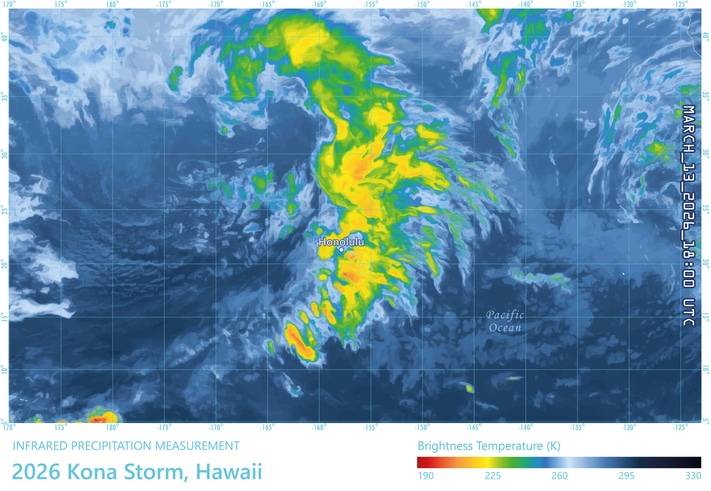

Hawaii Kona Storms Drive at Least $1 Billion in Losses, Aon Reports

March 31, 2026

INSTANDA MAX Launches to Enable AI-Powered, Large-Scale Underwriting for Commercial Insurers

March 31, 2026

IBHS and APCIA Release Wildfire Risk Reduction Framework for Communities

The Insurance Institute for Business & Home Safety and the American Property Casualty Insurance Association released a new toolkit on March 25, 2026, to help communities implement coordinated wildfire mitigation programs. The Community Wildfire Risk Reduction Program Framework provides structured guidance for local governments, fire services, and community organizations working to reduce wildfire risk.

The resource focuses on practical, science-based strategies to address home ignition and limit wildfire spread at the neighborhood level.

Framework Outlines Step-by-Step Community Planning

The toolkit provides step-by-step guidance for planning, designing, and launching local wildfire risk-reduction programs. It also includes tools to support long-term program sustainability.

In addition, the framework incorporates science-based home mitigation standards. These include structural hardening measures and defensible space requirements, such as maintaining a 0- to 5-foot noncombustible safety zone around properties.

The resource also provides assessment and training materials designed to support consistent property evaluations. These materials aim to help communities train home assessors and standardize mitigation practices.

Implementation Tools and Outreach Strategies Included

The framework includes practical implementation tools such as program checklists, sample forms, funding considerations, and administrative guidance. These resources are designed to help communities operationalize wildfire mitigation efforts.

It also outlines outreach and coordination strategies to engage homeowners, local partners, and supply chain providers. The goal is to encourage community-wide participation in risk reduction efforts.

Steve Hawks, senior director for wildfire at IBHS, stated that many communities now face wildfire as an ongoing risk. He said the toolkit provides a consistent, research-based approach that communities can use to reduce home ignition and strengthen neighborhoods.

Focus on Reducing Structure-to-Structure Fire Spread

The framework highlights the role of structure-to-structure fire spread in wildfire events. Unlike some natural disasters, wildfires can intensify when they move from wildland areas into neighborhoods. A single home ignition can lead to a chain reaction of fire spread between structures.

The toolkit emphasizes strengthening homes and creating defensible space across entire neighborhoods. These measures aim to reduce the likelihood of widespread destruction.

Karen Collins, vice president of property and environmental at APCIA, noted that wildfire risk remains a persistent issue. She said reducing the likelihood of home ignition from embers, flames, and extreme heat is critical. She also highlighted the importance of community-wide action led by local officials and supported by property owners.

Broad Industry and Fire Service Support

The framework has received support from organizations across wildfire mitigation, fire services, and the insurance sector.

The National Fire Protection Association contributed wildfire risk reduction information and messaging to the toolkit. Michele Steinberg, the organization’s wildfire division director, said the resource helps deliver critical mitigation information to communities.

California State Fire Marshal Daniel Berlant emphasized the role of community coordination. He stated that informed and connected communities can take meaningful action to reduce wildfire risk.

Oregon State Fire Marshal Mariana Ruiz-Temple highlighted the framework’s focus on evidence-based strategies, including home hardening and expanding defensible space.

Jessica Martinez of the California Fire Safe Council said tools that translate wildfire science into practical resources can support local mitigation efforts.

Chief Jeremy Craft of the Western Fire Chiefs Association noted that fire services cannot protect every structure during a wildfire. He said residents must take action before a fire occurs.

Mark Novak of the International Association of Fire Chiefs pointed to current weather conditions, including warm temperatures and low precipitation, as factors increasing wildfire risk. He said the framework provides clear guidance for community preparedness.

Insurance Industry Perspective on Mitigation Efforts

Insurance organizations also expressed support for the framework’s approach.

Kenton Brine, president of the NW Insurance Council, said insurers have promoted wildfire mitigation for more than a decade. He noted that the framework provides access to proven tools that help prevent the spread of fire in built environments.

Carole Walker, executive director of the Rocky Mountain Insurance Association, said the framework helps communities implement preparedness strategies that improve home safety and insurability.

Access to the Toolkit

Communities can access the full Community Wildfire Risk Reduction Program Framework through IBHS. The resource includes templates, guidance documents, and implementation materials designed to support local wildfire mitigation programs.

The IBHS conducts scientific research to identify effective actions that strengthen homes, businesses, and communities against natural disasters. APCIA serves as a national trade association representing property and casualty insurers across the United States.

Get the latest insurance market updates and discover exclusive program opportunities at ProgramBusiness.com.

March 30, 2026

Severe Convective Storm Risk Report 2026: Coordinating the Recovery Ecosystem

Severe convective storms, including hail, tornadoes, and straight-line winds, are now a primary driver of insured losses, according to Cotality’s 2026 Severe Convective Storm Risk Report. The report highlights how recovery outcomes depend on coordination across underwriting, modeling, claims, and restoration functions.

A fictional scenario illustrates the challenge. Two homeowners experienced hail damage, but delays in claims response allowed additional rain to cause mold and significantly increase total loss costs. This example reflects broader issues tied to response timing and resource availability.

A Multi-Stage Recovery Process

Cotality describes storm recovery as a coordinated effort across several roles:

- Underwriters use structure-level data for risk selection and pricing.

- Catastrophe modelers identify high-risk concentrations.

- Claims representatives verify events and initiate recovery.

- Restoration contractors complete repairs and reconstruction.

Each stage contributes to the speed of property restoration.

Underwriting and Exposure Trends

The report states that historical weather data alone is no longer sufficient. Insurers are incorporating forward-looking data, including building characteristics such as roof age and condition.

Hail remains a major driver of claims. Older roofs are more susceptible to damage, which can increase claim severity. Cotality estimates that more than 43.5 million U.S. properties fall into moderate or greater hail risk categories, representing $17.8 trillion in reconstruction cost value.

Texas leads in exposure with nearly 8 million properties and $3.1 trillion in risk. Illinois ranks second with $1.5 trillion. At the metro level, the Chicago area has the highest exposure at $1.0 trillion, referred to as the "Chicago Anomaly."

Catastrophe Risk and Hail Losses

The report identifies a shift in how severe convective storms are categorized. Previously considered secondary perils, these events now cause losses comparable to those from major hurricanes.

At a 500-year return period, modeled losses reach $71 billion, with a single hailstorm accounting for $58 billion. Even at more frequent intervals, hail events can generate nearly $30 billion in insured losses.

A June 2023 Texas storm cluster caused $7 billion to $10 billion in losses, with 95 percent attributed to hail. A shift of 15 to 20 miles into a denser area would have increased losses to approximately $30 billion.

Claims and Weather Verification

Claims response timing remains a key factor in recovery. Fast, accurate weather verification enables earlier resource deployment.

In 2025, hail measuring 2 inches or greater impacted more than 600,000 properties, representing $177 billion in reconstruction cost value. Texas recorded more than 235,000 impacted homes. Wyoming, Oklahoma, Wisconsin, and Kansas also reported high volumes, accounting for about 66 percent of affected properties.

Cotality recorded 142 days of damaging hail in 2025, exceeding the 20-year average of 122 days.

Restoration and Project Complexity

Restoration workflows are becoming more complex. Contractors manage multiple services, including emergency stabilization, water mitigation, contents restoration, and reconstruction.

Exterior damage to roofing, siding, and windows is common. In some cases, full structural rebuilding is required. Contractors are also expanding into appraisal and consulting roles to support cost estimation and documentation.

Storm-related water intrusion increases interior damage risk, often requiring mitigation work before claims are finalized. Large-scale events can also extend project timelines due to labor and supply constraints.

Global Activity

The report notes similar patterns internationally. In Europe, Germany recorded 12.3 billion EUR in losses from 2000 to 2024, while Ireland had the highest per capita losses.

A July 2023 storm system in southeastern Europe produced high winds, large hail, and flooding across multiple countries, causing structural damage and infrastructure disruption. The event placed simultaneous strain on multiple recovery systems.

Cotality’s report presents severe convective storm recovery as a coordinated process that relies on accurate data and alignment across industry functions.

Get the latest insurance market updates and discover exclusive program opportunities at ProgramBusiness.com.

March 30, 2026

Home Insurance Rates Are Climbing Again — What to Expect in 2026

Homeowners across the U.S. may face another year of rising insurance costs. A recent forecast from Insurify projects that home insurance premiums will increase by an average of 4% by the end of 2026, marking the fifth consecutive year of rate increases.

While the national average may seem moderate, some regions are expected to experience significantly higher jumps, driven largely by ongoing weather-related risks and rising claims costs.

What’s Driving Higher Home Insurance Costs?

The continued rise in premiums is closely tied to the growing frequency and severity of natural disasters.

Severe convective storms — including tornadoes, hail, and high winds — have caused widespread damage across the Midwest and Great Plains. In 2025 alone, these events resulted in more than $52 billion in insured losses, making it one of the costliest years on record.

Wildfires are also playing a major role, particularly on the West Coast. In Southern California, wildfires caused more than $250 billion in damages in 2025, further impacting insurers’ risk models and pricing strategies.

As these events become more common and more expensive, insurance companies are adjusting how they manage risk. This can lead to higher premiums, changes in coverage terms, or reduced availability in certain high-risk areas.

States Expected to See the Largest Increases

Although premiums are rising nationwide, some states are projected to see more significant increases in 2026:

- California: +16%

- Nebraska: +13%

- New Mexico: +11%

- Georgia: +10%

These projected increases follow sharp rate hikes in 2025 in states like Minnesota, Colorado, and Iowa, highlighting an ongoing trend in areas with elevated weather-related risks.

The Broader Impact on Homeowners

Rising insurance costs can influence more than just monthly expenses. Research from Florida State University suggests that a 10% increase in homeowners insurance premiums may lead to a 4.6% decrease in housing prices.

As affordability becomes a growing concern, insurance costs are increasingly part of the overall conversation around buying and owning a home.

The Most Expensive States for Home Insurance

Some states continue to stand out for their high insurance costs, often due to increased exposure to hurricanes, severe storms, or other natural disasters. According to projections for 2026, the most expensive states include:

- Florida: $8,458

- Oklahoma: $5,205

- Louisiana: $5,035

- Nebraska: $4,560

- Texas: $4,529

- Colorado: $4,164

- Alabama: $3,979

- Mississippi: $3,833

- Minnesota: $3,654

- Illinois: $3,559

Florida remains the most expensive by a wide margin, reflecting its ongoing exposure to hurricanes and coastal risks.

Where Rates May Decrease

Not all states are expected to see increases. Some areas may experience slight declines — up to 2% — by the end of 2026. These include:

- Hawaii

- Massachusetts

- Maine

- Louisiana

- Rhode Island

While these decreases are relatively small, they may provide some relief compared to the broader national trend.

What This Means Moving Forward

The steady rise in home insurance costs reflects larger changes in weather patterns, rebuilding expenses, and overall risk exposure. As insurers continue to adjust pricing and coverage strategies, homeowners may need to stay informed and regularly review their policies.

Understanding regional risks and how they impact insurance costs can help individuals make more informed decisions about coverage, property investments, and long-term planning.